Mortgage rates - what are the UK mortgage rates today?

UK mortgage interest rates can change quickly at the moment, depending on the current cost of swap rates, Bank of England (BoE) base rate announcements, and lenders' discretion.

In this article, we break down the current average mortgage rates in the UK for 2024 and look at the potential direction of future UK mortgage rates.

And if you're ready for a mortgage, our broker partner Mojo can help you find your best deal.

Stay in the know with the latest mortgage rates

Get the latest UK mortgage rates and deals straight to your inbox, from our broker partner Mojo Mortgages. All they need is your email address.

Best current mortgage rates

The table below shows some of the best two year fixed-rate mortgages and five year fixed-rate mortgages in the market right now, based on the lowest initial rate available at certain loan-to-value (LTV) ratios.

These might not suit you and your circumstances, but our partner Mojo can help you find the best mortgage deals that do.

Remember, you could lose your home if you don't keep up with your mortgage repayments.

- 2 years

- Fixed rate

- Monthly repayment£ 875.78

- Loan to value60 %

- Initial interest rate3.89 %

- Variable rate7.24 %

- APRC6.8%

- Product fees£ 1,132

Representative example:Repayment mortgage of £168,000.00 over 25 years, representative APRC 6.8%. Repayments: 29 months of £875.78 at 3.89% (fixed), then 271 months of £1,183.86 at 7.24% (variable). Total amount payable £346,223.68. Early repayment charges apply until 28-Feb-2027. Arrangement, mortgage discharge, valuation and CHAPS fees total £1132. Legal fees £117.43.

- 2 years

- Fixed rate

- Monthly repayment£ 1,049.77

- Loan to value70 %

- Initial interest rate4.14 %

- Variable rate7.74 %

- APRC7.3%

- Product fees£ 1,079

Representative example:Repayment mortgage of £196,000.00 over 25 years, representative APRC 7.3%. Repayments: 24 months of £1,049.77 at 4.14% (fixed), then 276 months of £1,449.87 at 7.74% (variable). Total amount payable £425,358.60. Early repayment charges apply until 2 years. Arrangement, mortgage discharge, valuation and CHAPS fees total £1079.

- 2 years

- Fixed rate

- £ 250 cashback

- Monthly repayment£ 1,229.93

- Loan to value80 %

- Initial interest rate4.39 %

- Variable rate8.54 %

- APRC7.5%

- Product fees£ 1,139

Representative example:Repayment mortgage of £224,000.00 over 25 years, representative APRC 7.5%. Repayments: 24 months of £1,229.93 at 4.39% (fixed), then 276 months of £1,743.84 at 8.54% (variable). Total amount payable £502,235.40. Early repayment charges apply until 2 years. Arrangement, mortgage discharge, valuation and CHAPS fees total £1139. Legal fees £105.

- 2 years

- Fixed rate

- Monthly repayment£ 1,457.06

- Loan to value90 %

- Initial interest rate4.9 %

- Variable rate7.24 %

- APRC7%

- Product fees£ 1,132

Representative example:Repayment mortgage of £252,000.00 over 25 years, representative APRC 7%. Repayments: 29 months of £1,457.06 at 4.9% (fixed), then 271 months of £1,790.29 at 7.24% (variable). Total amount payable £527,423.33. Early repayment charges apply until 28-Feb-2027. Arrangement, mortgage discharge, valuation and CHAPS fees total £1132. Legal fees £117.43.

The above deals are provided by Mojo Mortgages and updated every 12 hours. They may not be suitable for your circumstances and might not be available when you're ready to submit an application.

What are the current UK mortgage rates?

Current mortgage interest rates depend on the type of mortgage and your personal circumstances. For example, at the time of writing* average two-year fixed-rate deals range from 4.35% through to 5.63% depending on the size of your deposit and the lender criteria you match.

We look at the average mortgage rates across residential and buy-to-let mortgage deals in the UK below. While these can be useful for mortgage rate comparison and as a measure of what's happening in the market with regards to current UK mortgage rates, keep in mind that they are average mortgage rates.

This means that they won't necessarily be indicative of the full range of mortgage deals available in 2024 or of the lowest mortgages rates that you qualify for.

*23 September 2024

Average UK mortgage rates

The below mortgage rates are averages across the market, so do not show any individual lender rates that may be available. These averages are based on current mortgage deals and the latest UK interest rates available from over 70 lenders across the market.

Current average residential mortgage rates

A residential mortgage is one that you use for a property you plan to live in. The table below shows the average rates for selected deal lengths and types.

| Deal type and length | Current average rate across all lenders | Current average rate across big six lenders |

|---|---|---|

| 2 year fixed-rate (75% LTV) | 5.64% | 4.57% |

| 5 year fixed-rate (75% LTV) | 4.99% | 4.09% |

| 2 year variable rate (75% LTV) | 5.61% | 5.59% |

| Standard variable rate (SVR) | 8.49% | 7.25% |

All average rates are provided by Mojo Mortgages. The above are the average mortgage rates for various products across the market. These won't necessarily be available to you, and are not the only product types available.

Current average buy-to-let mortgage rates

A buy-to-let mortgage is usually used to purchase a property that you plan to rent out to others. The below table shows the average buy-to-let mortgage rates for selected deal lengths and types.

| Deal type and length | Average rate across all lenders | Average rate across big six lenders |

|---|---|---|

| 2 year fixed-rate mortgage (75% LTV) | 5.36% | 4.9% |

All average rates provided by Mojo Mortgages. The above are the average mortgage rates for a two-year fixed-rate (75% LTV) buy-to-let mortgage. These won't necessarily be available to you, and are not the only product types available.

It's important to note the above rates aren't necessarily indicative of the mortgage rate you would be offered.

The lowest mortgage rate you can get will depend on your financial circumstances and how much deposit you can put down. The bigger the deposit, the lower the loan-to-value (LTV) which generally allows you access to better mortgage rates - as lenders will see you as less risky.

In the current climate, it's worth speaking to a whole-of-market mortgage broker who can compare mortgages to find the right current mortgage rate for you.

Stay in the know with the latest mortgage rates

Get the latest UK mortgage rates and deals straight to your inbox, from our broker partner Mojo Mortgages. All they need is your email address.

How do mortgage rates work?

When you take out a mortgage, you're taking out a loan which you'll need to repay. In addition to the loan, you have to pay interest on the amount you borrowed. The amount of interest you pay is determined by your mortgage rate.

The higher the mortgage interest rate, the more expensive your monthly repayments will be. That's why it's good to compare mortgage rates and try to get a deal with the lowest mortgage rate possible and find the best mortgage rate for your personal circumstances.

Different mortgage rates work in slightly different ways:

Fixed-rate mortgages - won't change for the full length of the deal, usually two, three, five or 10 years. This can be great for budgeting, but won't allow you to take advantage if rates fall

Variable-rate mortgage deals - This includes discount mortgages and tracker mortgages. All variable rate deals can change at any time. For discount and trackers, this includes during the introductory period

Standard variable rate (SVR) - this is not a mortgage deal type, it's the lender’s default rate - so what you pay if you don't choose one of the deals or if your deal ends and you don't remortgage onto another one. A standard variable rate mortgage is usually set a couple of percent higher than any deals lenders offer, and as a variable mortgage rate, can also change at any time. However, there is no tie in period, so you can leave at any time

How does inflation impact mortgage rates?

Inflation is the rate at which the cost of goods rise over time. One of the most popular ways inflation is measured in the UK is by monitoring the monthly price changes across a range of products known as the Consumer Prices Index (CPI). When inflation is high, the Bank of England increases the base rate of interest in an attempt to curb inflation. If the cost of goods rise, this decreases the appetite to purchase goods, which eventually leads to prices, and therefor inflation, falling.

The base rate influences all mortgages, but has the most impact on variable rate mortgages, specifically a tracker, which tends to rise and fall directly in line with the base rate. Other variable rate mortgages (discount and standard variable rate) are also liable to change when the base rate does, but can really change any time at the lenders' discretion. If you're on a fixed-rate mortgage you won't see the impact of base rate changes in your mortgage interest rate until your deal ends.

Why are current mortgage rates so high?

Towards the end of 2023, average fixed mortgage rates were declining. They continued declining at the very start of 2024, however, it's very difficult to predict if they will continue to do so. This is why it's wise to compare mortgage rates regularly if you plan to take on a new deal.

From the end of 2021 until August 2023, the Bank of England increased the base rate 14 times in a row to 5.25%. This was to combat rising inflation, although UK inflation has recently fallen to its target level of 2%. The base rate was subsequently reduced in August 2024 for the first time since 2020, to 5%.

Swap rates have continued to change a lot in the last year, with some lenders changing fixed mortgage rates as a result. This has meant there has been continued volatility in the market despite the base rate remaining the same for much of the last year.

Will UK mortgage rates fall or rise in 2024?

The Bank of England's Monetary Policy Committee is next set to make a decision about whether to increase the base rate on 7 November 2024.

But it's important to note, changes to the base rate don't necessarily mean that mortgage rates will also change. While certain mortgage deals (tracker mortgages) have rates directly linked to the base rate, the rates on other types of mortgages are influenced by other factors in addition to the base rate, such as swap rates and the lender's discretion.

If you are due to remortgage, the average standard variable rate (which you're moved to after your current mortgage deal ends) is still above 8%, which is much higher than the average fixed mortgage rate.

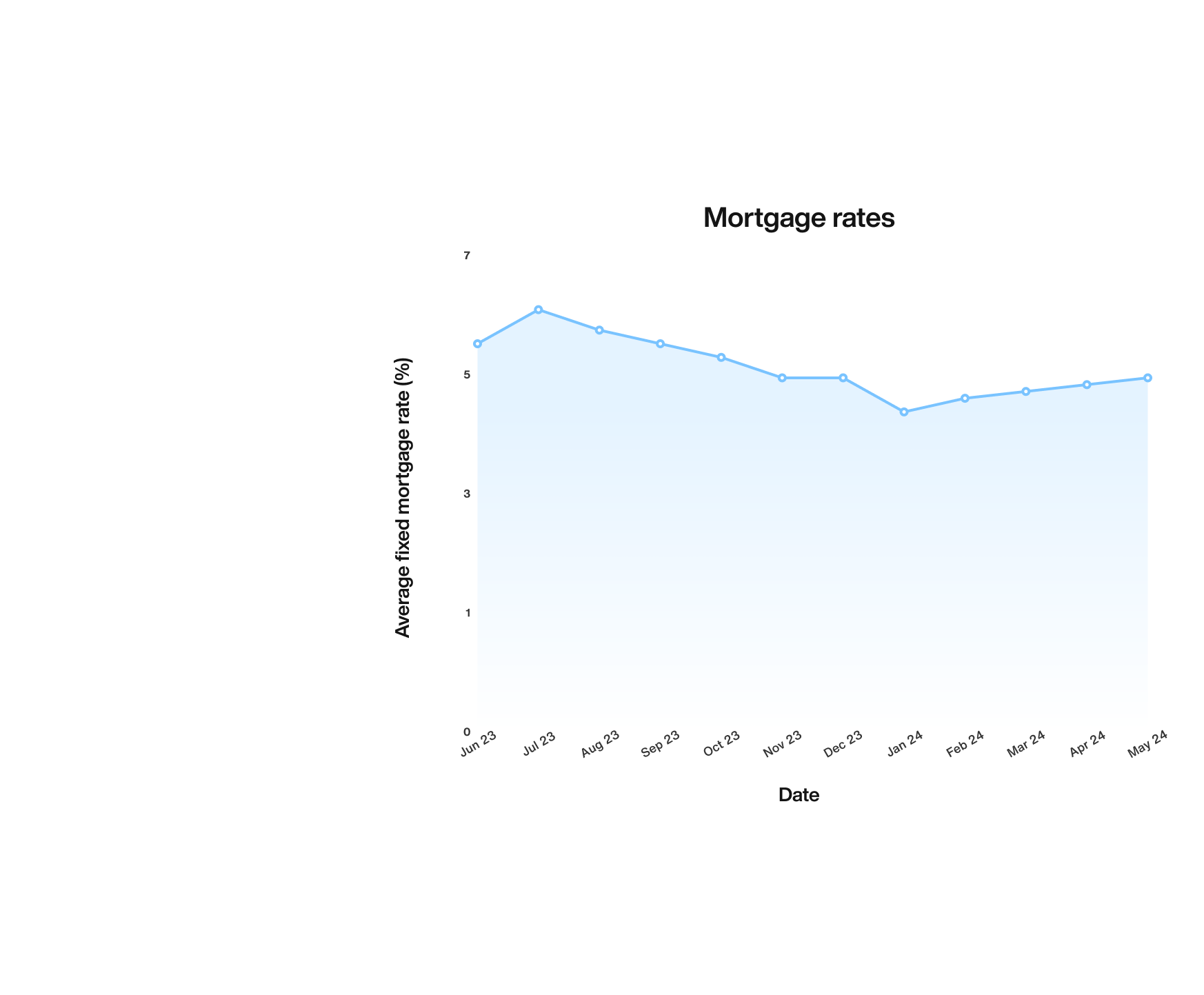

This graph shows how fixed mortgage rates changed over the course of 2023 due to various factors. At the beginning of 2024, rates fell but have started to rise again in recent weeks.

Source: Mojo Mortgages

What should I do if mortgage rates rise?

If you're concerned about your mortgage interest rate rising, then you may want to consider:

Fixing your mortgage – this will keep your rate the same for a set period of time. If your current mortgage deal hasn't ended, however, make sure you're aware of any early repayment charges (ERCs) when you compare mortgage rates

Secure a new interest rate today – if you're due to remortgage within the next six months, you can lock in a new rate now and switch when your mortgage deal ends, avoiding an ERC. If rates fall before your deal ends, you can switch again to get a better option

What should I do if mortgage rates fall?

if you're worried that interest rates will fall after you've secured a mortgage, you could:

Opt for a shorter-term fixed-rate mortgage deal – this means you're locked into that rate for less time

Consider a variable-rate mortgage, such as a discount deal – but keep in mind that if rates rise, you'll end up with higher monthly repayments

Stay in the know with the latest mortgage rates

Get the latest UK mortgage rates and deals straight to your inbox, from our broker partner Mojo Mortgages. All they need is your email address.

Customers also asked

How are mortgage rates determined?

When lenders determine mortgage rates they are usually making a best guess about what will happen with the UK base rate and guided by the movement of swap rates - the rate at which banks borrow money.

However, when the base rate changes, while tracker mortgages are directly impacted, fixed-rate mortgages won't necessarily be affected. This is because lenders tend to plan changes to their rates ahead of time when they think that the Bank of England are planning to adjust the base rate of interest.

Of course, there is also a business element to lender decisions, which means that they will also be trying to price their deals competitively in the market to attract more customers.

What is a good mortgage interest rate?

A good mortgage interest rate depends on market conditions, along with the size of your deposit and financial circumstances. It's a good idea to take this into consideration when looking at mortgage rate comparison, as not all deals will necessarily be available to you.

If you have a large deposit (ideally 40% or more) and excellent credit history, you should be able to get some of the lowest rates available. However, if have a small deposit and your credit rating isn't so strong, you'll likely find you have to pay a more expensive mortgage rate.

This is because lenders tend to base the rate on how much risk they're taking on by letting you borrow from them. The higher the deposit you put down, the lower the LTV ratio and less risk they're taking on. Similarly, if you have a great credit history, lenders are likely to see you as less of a risk. A mortgage broker can help you to compare mortgage rates and find the the most suitable for your circumstances.

How often do mortgage rates change?

It can be tough to compare mortgage rates as theoretically, they can change at any time based on a wide range of economic factors. If you're on a fixed-rate deal, you'll be protected from these changes until your deal ends. However, it's possible for rates to significantly rise or fall during your deal period, especially if it's a number of years.

Lenders tend to be guided by changes in the Bank of England base rate, and swap rates, however, these aren't the only reasons they might choose to raise or lower rates. The Bank of England generally announces base rate changes every 6 weeks, but can also arrange emergency meetings where necessary.

When will mortgage rates go down?

One of the most commonly asked question relating to mortgage rates is when they will come down. However, while average rates are often quoted in the press, it's important to understand that every lender sets their rates based upon their own best guesses. This is why in the same week we can see some lenders push their rates up and others cut them.

There are many factors that come into play when lenders determine mortgage rates, with the base rate and swap rates being major considerations. However, ultimately, even the most skilled financial analysts can only venture an educated guess of when mortgage rates are likely to fall across the board.

The best way to stay up to date with current average rates is to bookmark this page, and always ensure you speak to a mortgage broker who can help you find the best mortgage deals available.

Should I lock in a mortgage rate today?

It really depends on your circumstances. If you're already on, or about to fall onto a high SVR (standard variable rate), then you'll need to consider whether it's worth paying more interest while you wait to see whether rates fall further.

However, keep in mind that the market has seen significant volatility in recent years, and just because rates have fallen from their highest levels in recent history, the base rate remains high for the time being.

If you plan to move soon, then it may be worth staying on an SVR for a short time, as there are no ERCs to pay when you do look at a new mortgage deal. However, it's a good idea to take guidance from a broker on your mortgage comparison if you're uncertain on your best move.

Who offers the best mortgage rates?

There is no one lender that offers the 'best mortgage rates' across the board. While lenders tend to publish rates on some of their deals, it's worth keeping in mind that each deal will have its own set of criteria to meet in order to achieve that rate.

A significant factor will be deposit size, as rates tend to be set based on the loan to value (LTV) of your mortgage loan. Generally, the more deposit you have, the better UK mortgage rates available to you. However, a whole host of other factors come into play, such as your credit history, employment and even the property you plan to buy.

For this reason, it's a good idea to search the market to find those lenders with the best rate whose criteria you most closely match. A mortgage broker, like our broker partner, Mojo mortgages, can help you do this efficiently and reduce the possibility of missing out on a deal that suits you better.

Can you lock in a mortgage rate for 30 years?

It is possible to find 30 year, and even some longer fixed-rate mortgage deals than that in the UK these days. But this is typically far more common in the USA and Europe, as our longer-term fixed rate deals still tend to be fairly pricey, and hard to find.

However, there are multiple pros and cons to consider when it comes to locking in a mortgage deal for a very long time. It's a good idea to look at whether a long term fixed-rate mortgage is the right option for you, before tying in for 30 years.

How does the Bank of England Base Rate impact mortgage rates?

The Bank of England base rate is used by the organisation to help manage inflation. When inflation is low and they want to encourage borrowing and spending, the Bank of England will lower the base rate, as this make loans more affordable.

When they want to reduce inflation, the Bank of England will increase the base rate. The idea is that this will discourage spending and encourage saving. With mortgages, it depends on what kind of deal you have as to how base rate changes will affect your rate.

You can find out more in our guide to the Bank of England base rate.

Will 'Dutch-style' mortgages come to the UK?

Dutch-style mortgages are named as such based on similar mortgage products on the continent. The difference is that they provide longer fixed-term deals with interest rates that decline automatically as you pay the mortgage off.

This is intended to save time and money by reducing the need to regularly remortgage at the end of a fixed term. Not many UK lenders currently offer this type of product, however, if popular, there is always the potential that others will follow suit.

Should I wait until 2025 to buy a house?

If you're buying your first home, one of the most important factors is your personal financial circumstances. So while the market conditions, in terms of mortgage rates and house prices should also be a factor, it's a good idea to ensure you have a good deposit, and strong affordability regardless.

You can monitor house prices via Zoopla's monthly house price index, and keep up with what's going on in the UK mortgage world on our mortgage news page. However, ultimately, even in a peak buyers market, ensure you're in the best personal position too.

What’s the difference between the interest rate and APRC?

The mortgage interest rate is the amount you'll pay on top of what you borrow. This will be expressed as a percentage. The APRC, on the other hand, demonstrates the total cost payable throughout the full mortgage term, assuming it stays the same, as well as associated costs, such as fees. This is also expressed as a percentage and is intended to help borrowers compare deals with and without fees against each other.

Keep in mind that the APRC is only relevant if you never intend to remortgage, as it's calculated on the basis that you keep the same deal for the full duration of your mortgage.

Didn’t find what you were looking for?

Find out about other mortgages

Read some of our most popular guides

YOUR HOME/PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

Uswitch makes introductions to Mojo Mortgages to provide mortgage solutions. Uswitch and Mojo Mortgages are part of the same group of companies. Uswitch Limited is authorised and regulated by the Financial Conduct Authority (FCA) under firm reference number 312850. You can check this on the Financial Services Register by visiting the FCA website. Uswitch Limited is registered in England and Wales (Company No 03612689) The Cooperage, 5 Copper Row, London SE1 2LH. Mojo Mortgages is a trading style of Life's Great Limited which is registered in England and Wales (06246376). Mojo are authorised and regulated by the Financial Conduct Authority and are on the Financial Services Register (478215) Mojo’s registered office is The Cooperage, 5 Copper Row, London, SE1 2LH. To contact Mojo by phone, please call 0333 123 0012.