- Uswitch.com>

- Mortgages>

- Switch Mortgage - Change Your Mortgage Provider

Switch Your Mortgage Provider

Switching mortgages to a new lender is also known as remortgaging. You can also switch mortgage deals but stay with your existing lender - this is known as a product transfer. Homeowners switch mortgages for a number of reasons, though the most popular is to save money, particularly if your current mortgage deal is coming to an end.

Need help switching mortgage providers? Our broker partner Mojo can help you.

How we operate

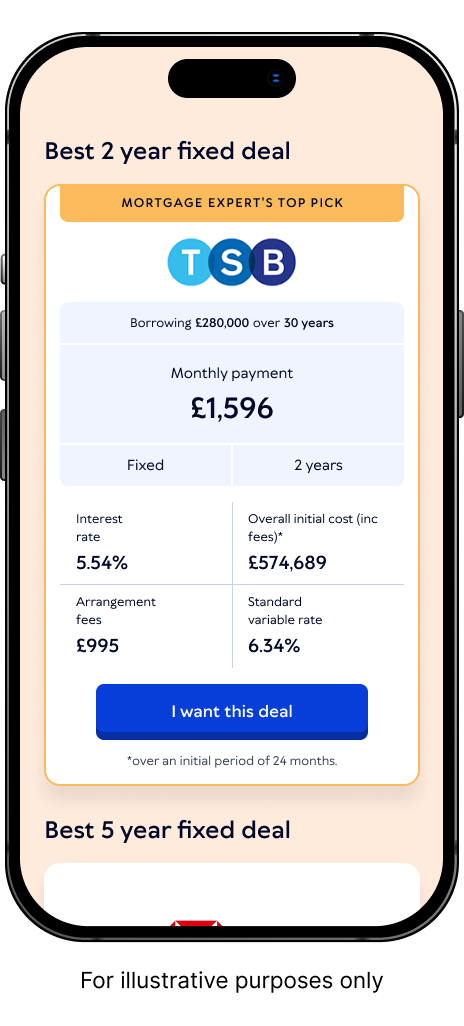

Our content is regularly reviewed by a team of our expert writers and our services are provided at no cost to you. Learn more about partnership content and how we make our money.

Here’s how to switch mortgages with us

Tell us your mortgage needs

Get a recommendation to switch from across many mortgage providers

Secure more than just a mortgage switch offer

Switch mortgage deals to one of 70+ lenders

YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

Why should I switch mortgage providers?

You might choose to change mortgage provider for lots of different reasons, including to:

Get a better mortgage rate - When you come to the end of your current mortgage term, you're transferred to the lender's standard variable rate (SVR) which is usually higher than any mortgage deals they have

Borrow more money - You may wish to remortgage to release equity when moving home to a more expensive property or as an alternative to a personal loan

Enjoy more flexible terms - You may want to take advantage of options offered by a different lender such as overpaying your mortgage, taking a payment holiday or offsetting your interest with an offset mortgage

Change deal type - You may want to switch from a variable rate mortgage to a fixed rate mortgage to be sure that your payments will remain the same for a set period. Or vice versa, if you feel that a variable rate offers you more flexibility

Benefit from a lower loan-to-value deal - If the equity you hold in your property has increased, either due to increased property value or repaying some of your loan, you may be able to take advantage of a lower loan-to-value (LTV) deal – which will likely come with better mortgage rates

When to switch mortgage providers

It's often worth looking at options around six months before the end of your existing deal. Most mortgage offers are valid for six months so you can secure a new deal and switch when your current deal ends, avoiding both the SVR and any early repayment charges (ERCs). However, if you're already on your lender's SVR, you won't face ERCs if you want to switch.

If you’re keen to switch sooner, before your existing deal ends, make sure you're aware of what fees will apply to remortgage early and check that the savings you'll make justify the cost. It can be worth consulting a fee free mortgage broker in this situation so you understand all your options.

When is it not a good idea to switch mortgage providers?

In certain circumstances, it may not be the right time to switch mortgage deals.

The ERCs are high – Unless you’re on an SVR, the chances are you'd have to pay to leave your mortgage deal. Early repayment charges can be high, so in many cases it may be better to wait until the fixed-rate deal comes to an end

Your financial circumstances have changed - If your financial circumstances or credit score have declined, it may not be possible to meet new lender requirements - especially if rates have also risen since you took out your original mortgage. In this case, you might find a product transfer (changing mortgage deals with your existing lender) more suitable

Your property has fallen in value – If your property's value has reduced since you bought it, the LTV (loan to value) of your borrowing may have risen

You have a small mortgage balance – If you owe less than £50,000 on your mortgage, switching to a new lender won’t necessarily be beneficial. The costs of a remortgage deal will likely cancel out any savings

You would prefer a cheaper and more straightforward option - A product transfer is typically easier and cheaper to arrange, so you may wish to explore changing mortgage deals with your current lender before settling on switching mortgage providers

Your existing lender offers better deals - Some lenders offer exclusive rates to existing mortgage holders, so it’s a good idea to check what mortgage deals are available from your current lender before looking elsewhere

When you're considering switching mortgages, timing is the most important factor. Your current circumstances will determine which deals are available to you, and therefore how much you could save. ”Laura Hamilton, Mortgage Expert

Customer Reviews

Super!

this was so easy and quick

Prompt and Helpful

Switching mortgage provider FAQs

How much does it cost to change mortgage providers?

There are a number of fees involved with remortgaging your property, namely:

Exit fees - Also known as a deeds release fee or mortgage completion fee, this is charged by some lenders to close your mortgage account. This charge typically applies no matter whether your deal has ended or not.

ERC (Early Repayment Charges) - Unless you're on your lender's SVR, you're likely to need to pay ERCs to leave your mortgage deal. This is generally charged as a percentage of what you still owe and can be very costly, especially if you have years remaining on your current deal.

Arrangement and booking fees - Not all lenders charge arrangement fees, but some banks and building societies will do.

Valuation and conveyancing - Your new lender will instruct a new valuation to gauge the current value of your property. Solicitors will also still have to carry out conveyancing and deed changes on your behalf, much like when you took out your original mortgage.

Many lenders offer fee free remortgages as an incentive to switch to them, meaning that valuation and legal fees won't always apply. Remember to compare mortgage deals across the market to make sure you get the best terms for your circumstances!

Is it worth switching mortgage providers?

It really depends on your exact circumstances. There are a lot of factors that contribute to whether or not a remortgage is right for you, and timing is key to this.

Switching to a new deal can save you money on interest, afford you more flexible terms, or even allow you to borrow more, but this won’t be true for everyone so it’s important to fully understand your choices.

Many people who took out mortgage before the Bank of England began raising the base rate back in 2022 may now find that the rates available to them are much less favourable, purely due to changes in the market, rather than their circumstances. That said, if you took out a two-year fixed-rate mortgage deal in mid-2023, you may find rates are becoming slightly more favourable now.

You may also find it more challenging to switch providers if your financial circumstances or credit score has declined, as the interest rates available to you may rise as a result or a new lender may even not be willing to accept your application.

If you plan to switch lenders, new mortgage affordability checks are likely to be carried out when you apply. However, this won't always be the case with a product transfer so you may be able to stick with your current mortgage lender even if you can't switch providers straight away.

If you're struggling to meet the affordability requirements to move mortgages with your existing lender too, it's best to seek the advice of an experienced mortgage broker.

How long does it take to switch mortgage providers?

A typical remortgage takes around four to eight weeks to complete. Depending on the complexity of the case, it can take a shorter or longer amount of time.

If you’re simply transferring your mortgage to a different deal with the same lender (a product transfer) it is usually much quicker.

How often can I switch mortgages?

You won’t usually be able to remortgage or do a product transfer within the first six months of taking out your mortgage, but you have the choice to switch mortgages at any point after that.

Remember that if you are currently in a fixed-rate mortgage deal or within the introductory rate period on a tracker or discount deal, you will likely have to pay ERCs (early repayment charges) to leave the deal before the term has ended. So if you keep leaving deals early and paying ERCs in order to get the best mortgage interest rate, the fees paid over the lifetime of the mortgage will likely outweigh the benefits you get from changing mortgage deals in the first place.

The best time to remortgage is typically when your current deal comes to an end, or when it otherwise makes financial sense to do so. You may wish to seek advice from a mortgage broker to make sure switching your mortgage is the best option for you.

Didn’t find what you were looking for?

Find out about other mortgages

Read some of our most popular guides

We’ve been featured in

YOUR HOME/PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

Uswitch makes introductions to Mojo Mortgages to provide mortgage solutions. Uswitch and Mojo Mortgages are part of the same group of companies. Uswitch Limited is authorised and regulated by the Financial Conduct Authority (FCA) under firm reference number 312850. You can check this on the Financial Services Register by visiting the FCA website. Uswitch Limited is registered in England and Wales (Company No 03612689) The Cooperage, 5 Copper Row, London SE1 2LH. Mojo Mortgages is a trading style of Life's Great Limited which is registered in England and Wales (06246376). Mojo are authorised and regulated by the Financial Conduct Authority and are on the Financial Services Register (478215) Mojo’s registered office is The Cooperage, 5 Copper Row, London, SE1 2LH. To contact Mojo by phone, please call 0333 123 0012.

*Average savings are based on Mojo Mortgages residential remortgage sales data, compared to the average SVR in February 2025. Actual savings will depend on individual circumstances.