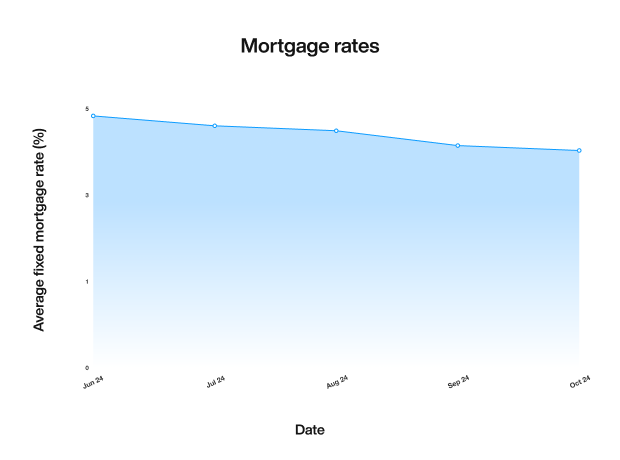

Remortgage rates today

Remortgaging in a high interest-rate environment can be daunting, especially if mortgage rates were much lower when you last took out a mortgage.

We look at how remortgage rates are influenced and how our broker partner Mojo can help you find your best remortgage deal.

How we operate

Our content is regularly reviewed by a team of our expert writers and our services are provided at no cost to you. Learn more about partnership content and how we make our money.

Current remortgage rates

The table below shows some of the best two year fixed-rate remortgages and five year fixed-rate remortgages in the market right now, based on the lowest initial rate available.

These might not suit you and your circumstances, but our partner Mojo can help you find deals that do.

Remember, if you don't keep up the repayments on your mortgage, you could lose your home.

- 2 years

- Fixed rate

- £ 250 cashback

- Monthly repayment£ 901.75

- Loan to value60 %

- Initial interest rate4.17 %

- Variable rate7 %

- APRC6.8%

- Product fees£ 1,224

Representative example:Repayment mortgage of £168,000.00 over 25 years, representative APRC 6.8%. Repayments: 28 months of £901.75 at 4.17% (fixed), then 272 months of £1,163.46 at 7% (variable). Total amount payable £341,710.12. Early repayment charges apply until 02-Apr-2027. Arrangement, mortgage discharge, valuation and CHAPS fees total £1224. Legal fees £184.75.

- 2 years

- Fixed rate

- £ 250 cashback

- Monthly repayment£ 1,079.50

- Loan to value70 %

- Initial interest rate4.42 %

- Variable rate7 %

- APRC6.9%

- Product fees£ 1,224

Representative example:Repayment mortgage of £196,000.00 over 25 years, representative APRC 6.9%. Repayments: 28 months of £1,079.50 at 4.42% (fixed), then 272 months of £1,360.01 at 7% (variable). Total amount payable £400,148.72. Early repayment charges apply until 02-Apr-2027. Arrangement, mortgage discharge, valuation and CHAPS fees total £1224. Legal fees £184.75.

- 2 years

- Fixed rate

- £ 300 cashback

- Monthly repayment£ 1,277.06

- Loan to value80 %

- Initial interest rate4.75 %

- Variable rate7.84 %

- APRC7.5%

- Product fees£ 1,705

Representative example:Repayment mortgage of £224,000.00 over 25 years, representative APRC 7.5%. Repayments: 27 months of £1,277.06 at 4.75% (fixed), then 273 months of £1,673.83 at 7.84% (variable). Total amount payable £491,436.21. Early repayment charges apply until 28-Feb-2027. Arrangement, mortgage discharge, valuation and CHAPS fees total £1705. Legal fees £258.

- 2 years

- Fixed rate

- Monthly repayment£ 1,486.41

- Loan to value90 %

- Initial interest rate5.09 %

- Variable rate7.84 %

- APRC7.5%

- Product fees£ 210

Representative example:Repayment mortgage of £252,000.00 over 25 years, representative APRC 7.5%. Repayments: 27 months of £1,486.41 at 5.09% (fixed), then 273 months of £1,887.56 at 7.84% (variable). Total amount payable £555,436.95. Early repayment charges apply until 28-Feb-2027. Arrangement, mortgage discharge, valuation and CHAPS fees total £210. Legal fees £258.

The above fixed rates are provided by Mojo Mortgages and updated every 12 hours. THEY MAY NOT BE AVAILABLE WHEN YOU'RE READY TO SUBMIT AN APPLICATION.

How to find the best remortgage rates

It's a good idea to look at the latest remortgage rates carefully before you decide to switch mortgages.

Our broker partner, Mojo Mortgages, can help you assess the remortgage options available to your carefully, and find your best remortgage deal, once you're ready to lock in a new rate. However, keep in mind that the best deal available to you won't always be the cheapest on the market.

How to get the cheapest remortgage rates available

When remortgaging, the rates available to you are very much based on your current circumstances. This comes down to:

Your current LTV - the lower it is, typically the lower the rate available

Your purpose for the remortgage - usually the lowest remortgage rates are available to those switching deals. If you're remortgaging to release equity (borrow more) then both your LTV and the risk in lending are increased

Your current financial circumstances - If your affordability has increased due to a higher income then this will also help reduce the risk of lending to you

Current credit score - If your credit rating has improved since you took out your mortgage, you'll usually be able to get lower rates than if it had declined

Keep in mind that lenders will look at these elements in unison, and each assess them differently, so to ensure you're getting the best deal available to you, it's best to speak to a broker.

What affects remortgage rates?

Much like when you took out your original mortgage, having the lowest loan to value (LTV) will typically give you access to the best remortgage rates. When it comes to remortgaging, your LTV is determined by your equity.

Equity is the difference between the current value of your home and how much you owe on your mortgage, so is determined both by the amount you've repaid and whether your property has increased or reduced in value.

As well as your LTV, lenders also assess your overall circumstances when considering the remortgage deals you qualify for. This includes your credit history, affordability of the new mortgage repayments and the purpose of your remortgage. You'll usually pay a higher rate on your remortgage if you're borrowing more versus purely switching to a new deal.

Why are remortgage rates higher?

Remortgage rates are not necessarily higher than purchase mortgage rates. For many people who took out their mortgage when interest rates were lower generally, it will feel like remortgage rates are much higher.

However, this is due to changes in the market. If interest-rates are lower across the market when you remortgage than when you buy your property, your remortgage rates would likely be cheaper.

Do you get a better rate when you remortgage?

Even in a high interest-rate environment, it's still possible to remortgage onto a lower rate than you're currently on.

This is because lenders base mortgage rates on LTV, and customers who have been repaying their mortgage for a number of years will typically have reduced the LTV of their borrowing. Although this can vary depending on property value and the interest rates you've been paying since your purchase.

Remortgage customers are often able to get better rates than would be available on the equivalent purchase mortgage loan, due to having greater equity than the average first-time buyer.

This is because a first-time buyer's LTV is purely based on their initial deposit, whereas a remortgage customer's LTV is based on their initial deposit as well as how much they have repaid to date, and any potential increase in property value.

Customer Reviews

A very positive experience

Very responsive

Great overall experience

About the author

We’ve been featured in

YOUR HOME/PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

Uswitch makes introductions to Mojo Mortgages to provide mortgage solutions. Uswitch and Mojo Mortgages are part of the same group of companies. Uswitch Limited is authorised and regulated by the Financial Conduct Authority (FCA) under firm reference number 312850. You can check this on the Financial Services Register by visiting the FCA website. Uswitch Limited is registered in England and Wales (Company No 03612689) The Cooperage, 5 Copper Row, London SE1 2LH. Mojo Mortgages is a trading style of Life's Great Limited which is registered in England and Wales (06246376). Mojo are authorised and regulated by the Financial Conduct Authority and are on the Financial Services Register (478215) Mojo’s registered office is The Cooperage, 5 Copper Row, London, SE1 2LH. To contact Mojo by phone, please call 0333 123 0012.